[ad_1]

Current market fads– consisting of a renovation in home mortgage prices, real estate price and prospective re-finance chances– recommend favorable indications for the realty market this year, according to February’s Home loan Display record from Intercontinental Exchange (ICE).

Home loan prices held at 6.71% since Jan. 24, down greater than a complete percent factor considering that their height in October, the record kept in mind. The spread in between the 30-year set home mortgage price and the 10-year Treasury return tightened to 253 basis factors (bps) on Jan. 24, dropping 18 bps considering that very early January and down around 50 bps from August.

On HousingWire’s Mortgage Rate Center, the 30-year adapting taken care of mortgage rate went to 6.908% since Feb. 5.

The ICE Home Consumer Price Index for December reported a yearly development price of 5.6%, up from 5.1% in November, which initially glimpse recommends a speeding up real estate market.

This velocity, nevertheless, is a recurring result of last springtime and summer season’s solid run of development, with even more current information recommending that the development price will certainly start to cool down in the coming months, the record kept in mind.

The seasonally changed regular monthly development price of home costs got from 0.09% in November to 0.13% in December. Yet rate gratitude stays trendy, dropping 0.42% in the month on a non-adjusted basis, well listed below the 25-year December standard of -0.08%.

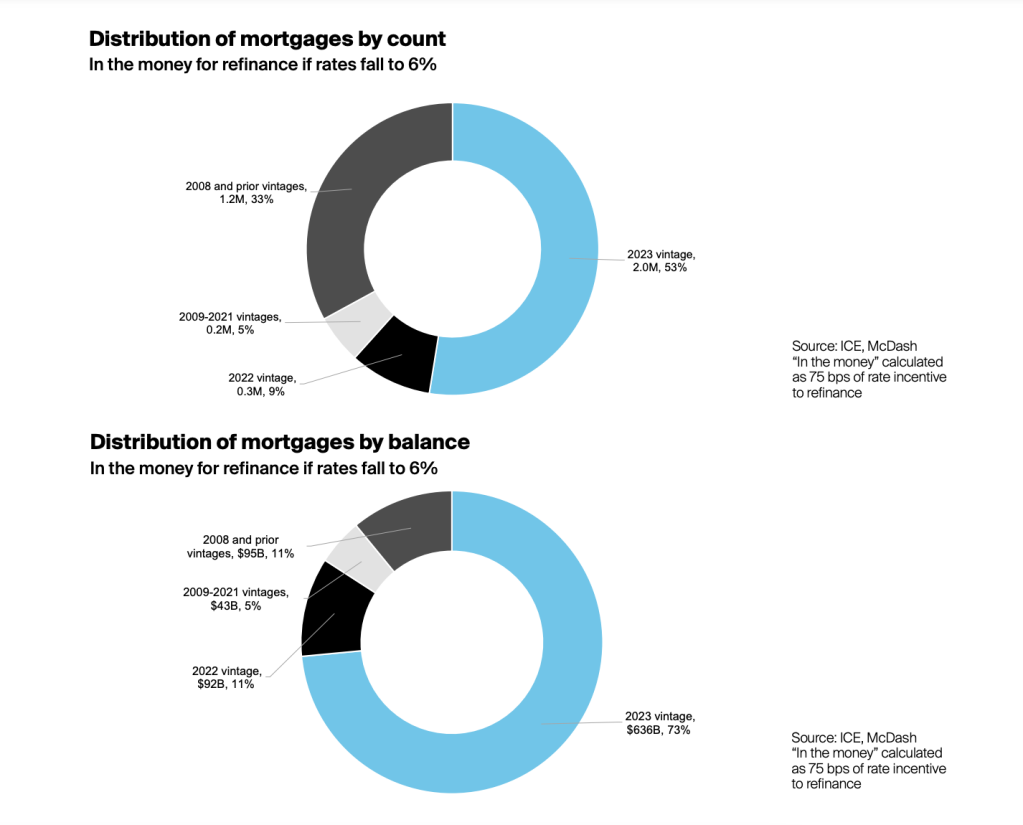

Re-finance Motivation

Reduced rates of interest have actually additionally started to gradually enhance re-finance motivations for existing house owners, especially amongst the 4.3 million home mortgages came from 2023.

Of the 2023 vintage, 2 countless these customers (or 26%) would certainly have the ability to reduce their first-lien price by 75 bps if 30-year prices are up to a forecasted 6% by the end of 2024, with 33% able to conserve a complete percent factor or even more.

” Under that circumstance– a prospective needle moving company for the re-finance market– some 46% of 2023-vintage customers would certainly be ‘in the cash,’ with virtually a 3rd able to reduce a complete percent factor off their present prices,” stated Andy Walden, ICE vice head of state of business study method.

If 30-year prices are up to 6% by the 4th quarter, as the Mortgage Bankers Association (MBA) and Fannie Mae are presently predicting, the total populace of lendings with a 75-bps refi motivation would certainly greater than double from 1.7 million to 3.8 million. Virtually 60% of that development would certainly originate from lendings come from 2023, ICE forecasted.

Under such a situation, over half would certainly be house owners that funded in 2023, with much less than 10% originating from 2022-vintage lendings.

One more one-third would certainly be customers that obtained lendings greater than 15 years back and did not re-finance when prices dipped listed below 3%, making them not likely to refi at 6%.

Home price

ICE kept in mind that home price has actually enhanced in current months regardless of a small higher tick in home mortgage prices over the previous couple of weeks.

Property owners are called for to make a month-to-month settlement of $2,257 to acquire the median-priced home, presuming making use of 30-year fixed-rate financing and a 20% deposit. That number is down $243, or virtually 10%, from a document in October, however up $831 (58%) from the beginning of 2022.

At 33.4% of the mean house revenue, the typical settlement is below a 38-year high of greater than 38% in October.

Yet that number is still 9 percent factors over the 30-year typical debt-to-income proportion of 24.2% and a little much less than the 33.8% height before the real estate market decline in 2006.

” If present sector price projections pertain to fulfillment, price will progressively enhance as we relocate with 2024 however remain to run more than long-run standards throughout the year,” the record mentioned.

Equity degrees

Home loan owners finished 2023 with $16 trillion in equity, the highest possible year-end overall on document, and up $1.6 trillion, or 11%, contrasted throughout of 2022.

Regarding $10.3 trillion of this overall is thought about “tappable,” indicating it can be taken out while preserving an 80% or reduced mixed loan-to worth (CLTV) proportion. This number increased by 12%, or $1.14 trillion, in 2023.

The typical home mortgage owner currently has $299,000 in equity, up from $274,000 at the end of 2022. This relates to approximately $193,000 in equity that might be taken out while still preserving a 20% equity risk in their home.

” Historically high degrees of equity remain to assist protect home mortgage capitalists from prospective losses and develop the problems for an increase in equity financing when rates of interest reduce sufficient to make withdrawals a lot more eye-catching to house owners,” according to the record.

Relevant

[ad_2]

Source link