[ad_1]

John Toohig, head of whole-loan buying and selling on the Raymond James whole-loan desk and president of Raymond James Mortgage Co., mentioned most of the identical headwinds the market confronted in 2023 stay as we roll into 2024. He mentioned amongst them are greater charges (down a bit at yearend, however nonetheless within the excessive 6% vary); “… the shortage of liquidity within the banking sector; more and more challenged affordability; and [consumer] credit score beginning to present some early cracks on the decrease finish of credit score and with youthful debtors.”

Nonetheless, an interest-rate drop and smooth touchdown for the financial system, if the latter is really achieved, will break a number of the ice in a relaxing housing market.

“For 2024, ought to the Federal Reserve decide they’ve overcorrected and begin to decrease charges [as indicated at the Fed’s December Federal Open Market Committee meeting], you will notice a surge in buying and selling volumes,” he added. “Reductions shall be much less impactful, loans will commerce nearer to par or features once more, and far of the frozen underwater coupons will transact once more.

“Ought to credit score break and the patron buckle, [however,] you could possibly see house costs fall, delinquencies and charge-offs on the rise and that can negatively influence pricing in a market with restricted liquidity.”

It stays a guestimate recreation so far as when the Federal Reserve — which paused charges at its ultimate assembly in 2023 — will resolve to start rolling again its benchmark fee within the 12 months forward from the current range of 5.25%-5.5%.

As 2023 moved towards an in depth, 30-year fastened charges had dropped into the mid-to-high 6% range. Few, if any, business teams or market specialists, nevertheless, have been correct in predicting charges very far out within the present topsy-turvy market.

“When you look at futures, you’re decrease [Fed] charges by Could of subsequent 12 months,” mentioned Tom Piercy, chief progress officer at Incenter Capital Advisors (beforehand Incenter Mortgage Advisors). “I wouldn’t make a guess on it’s as a result of there’s simply a lot complexity on this.”

MSR sector

Piercy, whose retailers advises each banks and nonbanks on mortgage servicing rights (MSRs) transactions, mentioned the 12 months forward for MSRs shall be impacted negatively if charges decline, however he provides charges must modify downward considerably to speed up loan-prepayment speeds, which might draw down the worth of MSR packages. He mentioned marginally decrease charges would have an effect on the returns holders of MSRs get from parked escrow accounts, nevertheless, which does influence MSR pricing.

Piercy expects that the mixed MSR buying and selling quantity within the coming two years (2024 and 2025) shall be on par with or barely higher than the mixed buying and selling quantity of 2022 and 2023, when charges spiked and greater than $1 trillion in MSR offers transacted every year.

“Over the subsequent three years, together with 2023, [we estimate] sub-$4 trillion [in MSR trades], perhaps within the excessive $3 trillion [range], and once more that’s for 2023 via 2025,” Piercy mentioned. For 2023, barely larger than 1.1 trillion in MSRs are anticipated to have traded, he added.

A part of that buying and selling quantity in 2024, Piercy mentioned, is anticipated to be pushed by MSR gross sales ensuing from the persevering with merger and acquisition (M&A) exercise within the nonbank sector of the market.

“Except there’s some sort of pickup within the forecast for originations, I feel you’re going to see nonetheless an lively M&A market via 2024,” he defined. “Many retailers will most likely look to grow to be half of a bigger, extra financially secure platform.

“We’re forecasting proper now a reasonably robust Q1 for MSR gross sales. I feel it’s going to be a sturdy market.”

MBS sector

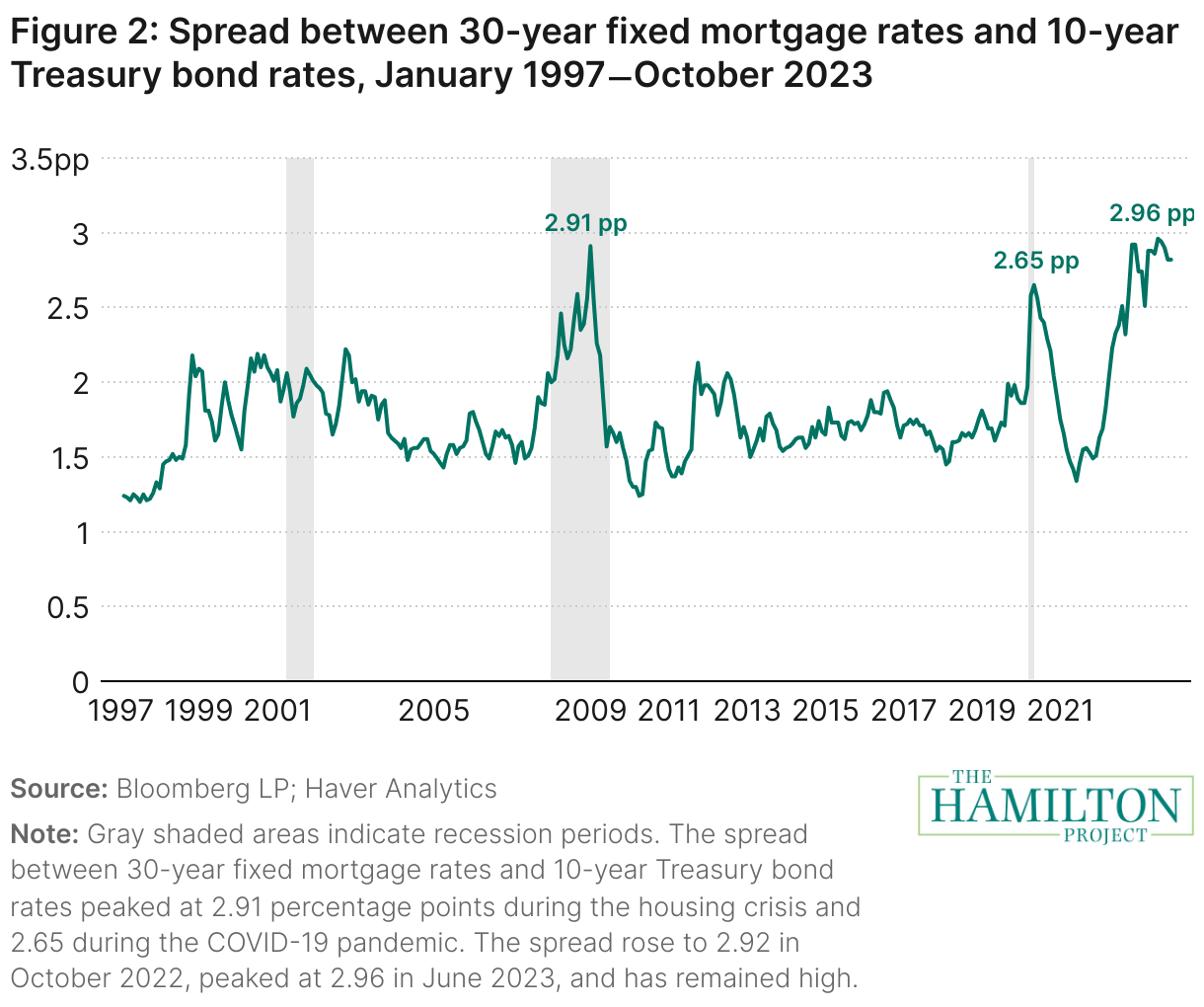

Sturdy is just not the adjective to explain what’s forward in 2024 for the company (Fannie Mae, Freddie Mac and Ginnie Mae) mortgage-backed securities (MBS) market, nevertheless. Market observers say outsized spreads between the 30-year fastened mortgage fee and 10-year Treasuries and subpar MBS clearing charges are prone to proceed, given the imbalance in supply and demand out there because the Federal Reserve continues to unwind its $2.5 trillion portfolio of MBS.

{kind=link}

In response to projections by actual property funding agency the Amherst Group, company MBS internet issuance for 2024 is estimated at $300 billion, up barely from $250 billion in 2023 — however nonetheless down considerably from the barnburner 12 months in 2021, when internet issuance totaled $870 billion. Web issuance in MBS represents new securities issued much less the decline in excellent securities resulting from principal paydowns or prepayments.

The Federal Reserve’s ongoing quantitative easing is anticipated to contribute an extra MBS provide to the market in 2024 of some $225 billion, which is able to must be absorbed along with the projected $300 billion in internet new issuance.

“Usually, our view has been that mortgages are actually undervalued,” mentioned Amherst Chairman and CEO Sean Dobson. “I’ve been doing this for 30 years, they usually’re about pretty much as good in worth as they’ve ever been.

“However we don’t see lots of snapback, with mortgages getting again in line [in terms of interest rates] anytime quickly. … Mortgage charges are excessive and one massive cause … is the [agency MBS] investor base is impaired, and it’s not prone to be fastened quickly.”

Dobson added that, in his view, monetary policymakers didn’t absolutely grasp that when the Fed stopped shopping for mortgages, “that they had displaced the precise consumers for thus lengthy that the precise consumers at the moment are gone.

“… Now you should buy billions of {dollars} in bonds [MBS] which are actually undervalued relative to their intrinsic danger as a result of there’s simply no sponsor [a major new buyer since the Fed’s pullback].”

Richard Koss, chief analysis officer at mortgage-data analytics agency Recursion, additionally presents a bleak evaluation of the company MBS market forward — primarily as a result of mortgage originations are prone to stay depressed, which implies company MBS issuance shall be depressed as nicely.

Koss factors to the large quantity of low-rate mortgages excellent because the vexing downside the market faces, including that low-rate legacy (2020 and 2021) mortgage-backed swimming pools “are principally low cost bonds within the present [high] fee atmosphere.”

“All of the 4.0% and decrease mortgages that dominate the market are lower than 4 years previous,” he mentioned. “If in case you have a 3% mortgage, you want a 2.5% fee to justify refinancing, which is a 1% Treasury yield.

“That would occur, however we don’t need it to, because it means some type of catastrophe. I feel a mortgage winter has frozen issues exhausting and circumstances are such that we will solely count on a measurable enchancment out previous 2030.”

The Mortgage Bankers Affiliation (MBA) estimates that whole mortgage originations in 2023 will are available at about $1.6 trillion, down significantly from the $4.4 trillion in originations chalked up within the banner 12 months of 2021. Subsequent 12 months, the MBA forecasts whole originations at barely greater than $2 trillion — and its most current origination forecast exhibits solely modest enchancment in 2025, with originations (buy and refinance) reaching $2.43 trillion.

RMBS sector

The origination downturn and fee volatility in 2023 negatively impacted the private-label residential mortgage-backed securitization (RMBS) market. Many market specialists, nevertheless, count on a tailwind of declining charges for the 12 months forward on account of latest alerts from the Federal Reserve that fee cuts are on the desk, beginning as quickly as the tip of the primary quarter of 2024.

“Further fee hikes not look like a part of the dialog, MBA senior vp and chief economist Mike Fratantoni mentioned in an announcement reacting to the newest Fed fee determination. “It’s all in regards to the tempo of cuts from right here.

“…We count on that this path for financial coverage ought to assist additional declines in mortgage charges, simply in time for the spring housing market. We’re forecasting modest progress in new and current house gross sales in 2024, supporting progress in buy originations, following an awfully gradual 2023.”

A report revealed in late November by Kroll Bond Ranking Company (KBRA) — which tracks RMBS choices throughout the prime, nonprime, credit-risk switch and second-lien sectors (RMBS 2.0). — assumed that the Fed was “nearer to peak rates of interest.” That assumption bodes nicely for the private-label market in 2024 — relative to its performance in 2023.

“We count on 2024 circumstances to be extra favorable and RMBS 2.0 issuance ranges to be barely greater than in 2023 at $56.5 billion (a 9% improve),” the KBRA report states.

Andrew Rhodes, senior director and head of buying and selling at Mortgage Capital Buying and selling, mentioned the winter months forward are going to be tough going for the housing market, together with RMBS issuance.

“I feel 2024 [overall] goes to be higher from a [loan] origination standpoint, however I don’t assume it’s going to be massive improve,” he added. “…I actually do assume that 2025 shall be lots higher, however that’s fairly far ahead.”

Tailwinds

On a brighter observe, Ben Hunsaker, portfolio supervisor targeted on securitized credit score for Seashore Level Capital Administration, factors to the enlargement of second-lien merchandise within the main market as a loan-origination and RMBS volume-driver in 2024, given the record-levels of home equity out there to householders, a lot of whom at the moment are locked into low-rate mortgages and have little incentive to promote or purchase a brand new home.

“There’s this big pool of second liens and HELOCs [home equity lines of credit] that a number of the originators have began to make use of as a key a part of their toolkit, and also you’re listening to them speak about it on earnings calls,” he mentioned. “And so, I feel that most likely places a kick within the pants to what 2024 [RMBS] volumes might appear like.”

Charley Clark, a senior vp and mortgage warehouse finance government at EverBank (previously referred to as TIAA Financial institution), additionally strikes a observe of optimism for 2024 in terms of the prospects for housing business, particularly the big impartial mortgage banks (IMBs) that feed the origination and securitization pipelines. Clark notes that EverBank serves about 40 of the most important mortgage banking firms within the nation.

“I feel there’s positively nonetheless a number of the mom-and-pop retailers [IMBs] — or let’s say an organization with $20 million or $25 million or under in adjusted tangible internet price — that shall be seeking to promote,” he mentioned. “However many of the massive firms have strong steadiness sheets and have began to really cease the bleeding.

“I’m inspired as a result of these firms [large IMBs] are a lot better positioned now. They’ve made the cuts, a minimum of many of the cuts they should make to right-size for the place the business is heading. And the most effective firms have actually finished a superb job of that, so that they’re positioned to do nicely subsequent 12 months, but it surely’s nonetheless going to be powerful.”

[ad_2]

Source link