[ad_1]

In 2022, lots of recessionary warnings turned up. Nonetheless, after Nov. 9, 2022, a crucial recessionary information line transformed as mortgage rates dropped, brand-new home sales expanded, building contractors acquired down prices and the cycle carried on. You can see this in the building contractors’ self-confidence information.

In 2015, as prices increased toward 8%, the building contractors’ self-confidence dropped, and after that, as prices dropped, their self-confidence increased once again. One of the most current NAHB survey reveals building contractors’ self-confidence has actually delayed, and it will certainly probably head reduced quickly! Why has this taken place?

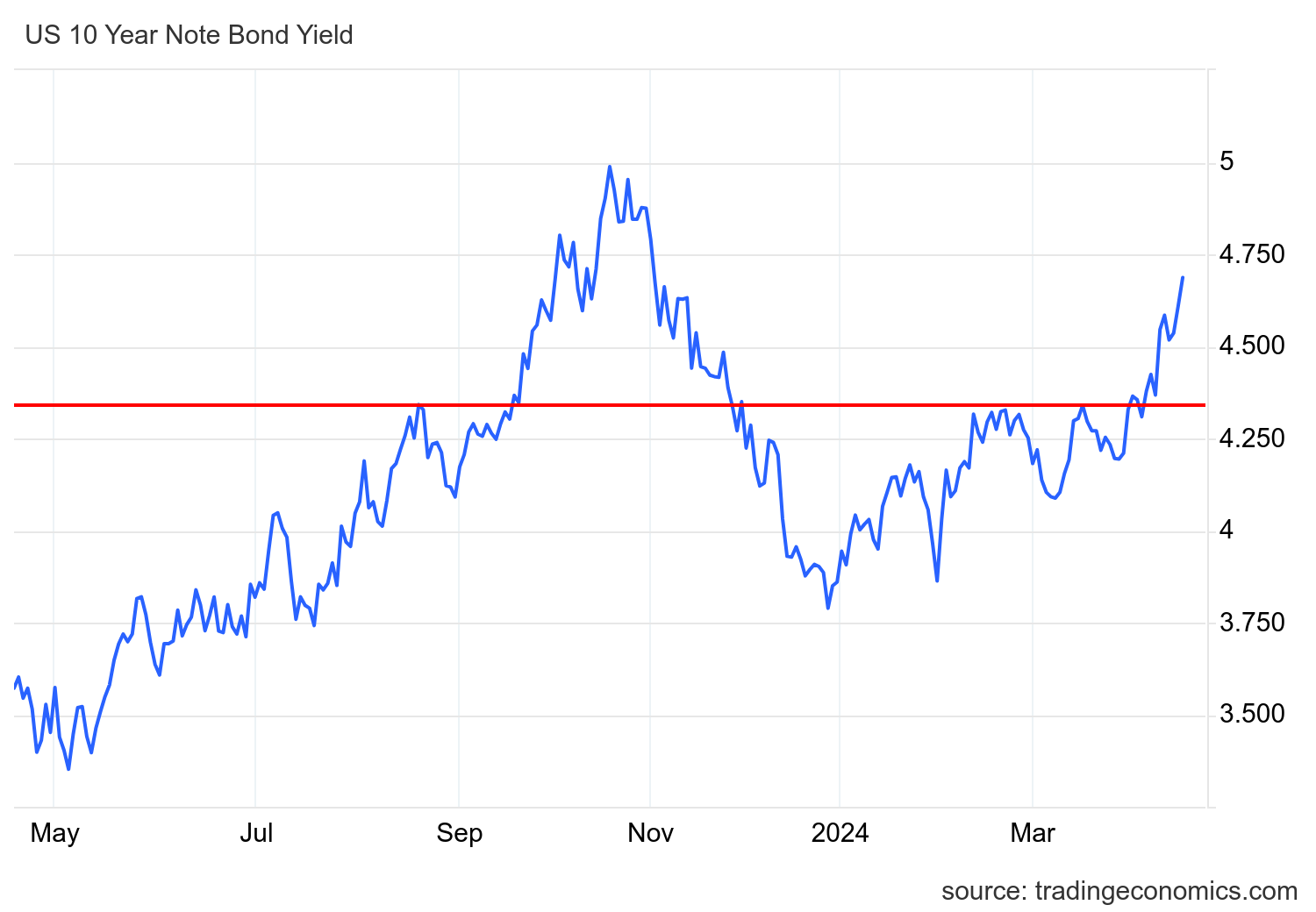

The 10-year return damaged a crucial assistance line recently, much like in 2014, and it wishes to examine 5% once again. It’s presently at 4.65%. This implies home mortgage prices are greater than they have actually been all year, and, as I spoke about last year on CNBC, greater home mortgage prices are never ever advantage for real estate.

I have not been a Fed pivot individual given that 2022– I do not assume the Fed will certainly pivot up until the labor market breaks. I lately reviewed just how high home mortgage prices can enter the HousingWire Daily podcast.

So, just how should we come close to the real estate begins information to comprehend when a work loss economic crisis will take place? Follow this trip with me.

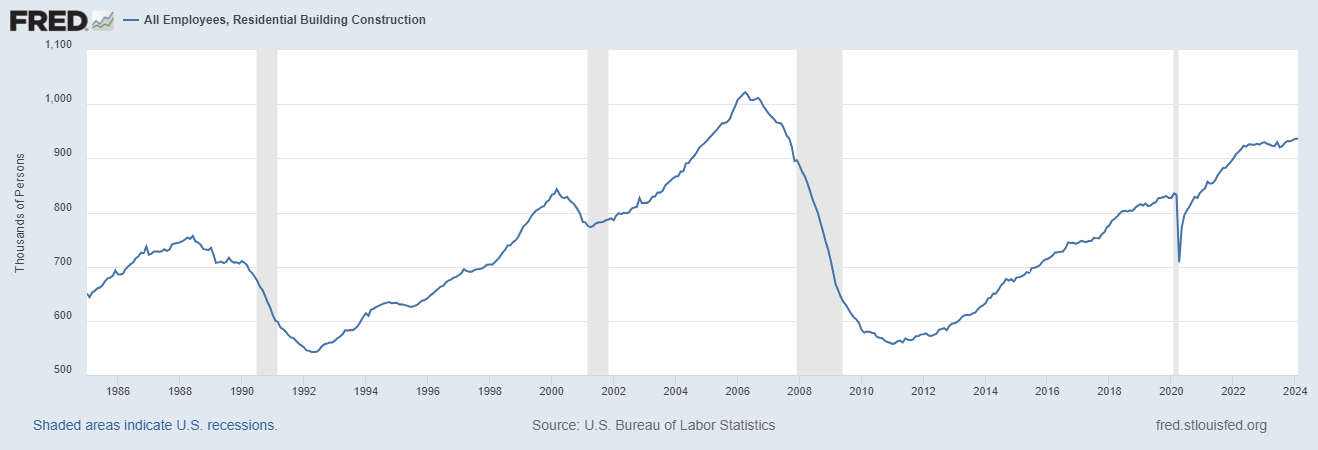

As we can see below, economic downturns generally do not begin up until household building and construction work are shed. This isn’t simply individuals that operate in homes and single-family homes, as redesigning work is likewise high below. As we can see below, we have not lose household building and construction work yet, and we have not entered into a work loss economic crisis either. Additionally, remember we are an aging culture, and infant boomers leave the labor force every month. Lots of firms bear in mind maintaining the correct amount of labor in their labor force.

Residential employees drop prior to the economic crisis as greater prices attack.

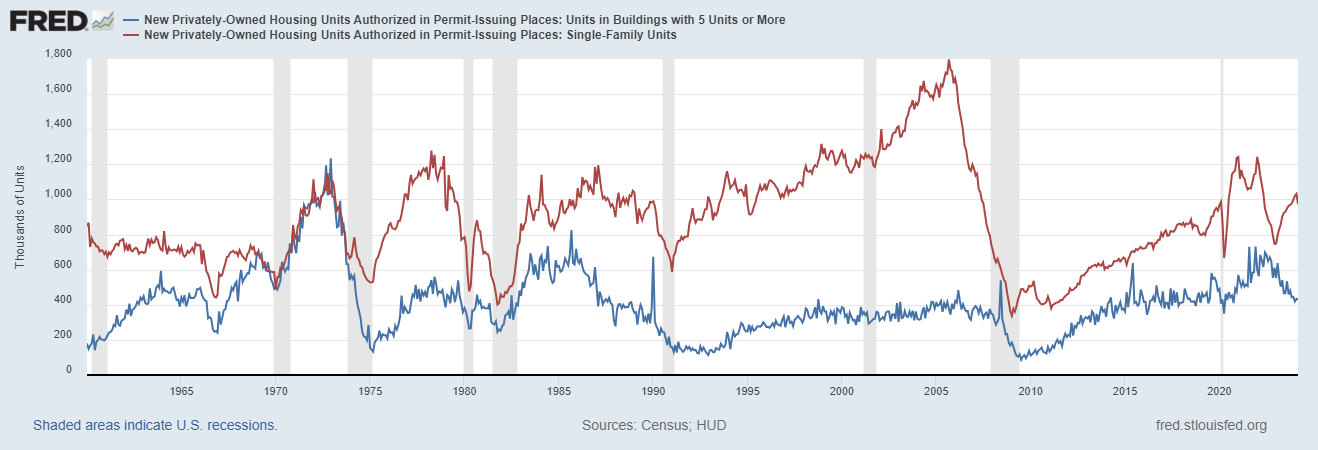

Currently, allow’s take a look at real estate allow information. As we can see in the graph below, 5-unit authorization information is currently at the reduced degrees of the COVID-19 economic crisis. As insane as this seems, we likewise have a shot at having this information line get to Great Financial Economic downturn lows.

Given That January 2023, as 5-unit authorizations have actually dropped, single-family authorizations have actually climbed. However that’s not what we see in this record: single-family authorizations dropped in this record. As we can see below, when both information lines drop with each other in time, it ultimately brings about building and construction employees shedding their work and out of work insurance claims increasing, which is just how each economic crisis has actually functioned.

We are not in the threat area yet, as we have a large stockpile of building and construction job that requires to be completed. Nonetheless, I am producing a path for you to stroll to in the future.

* Notification just how allows for single-family and 5 devices have a tendency to drop with each other prior to the economic crisis.

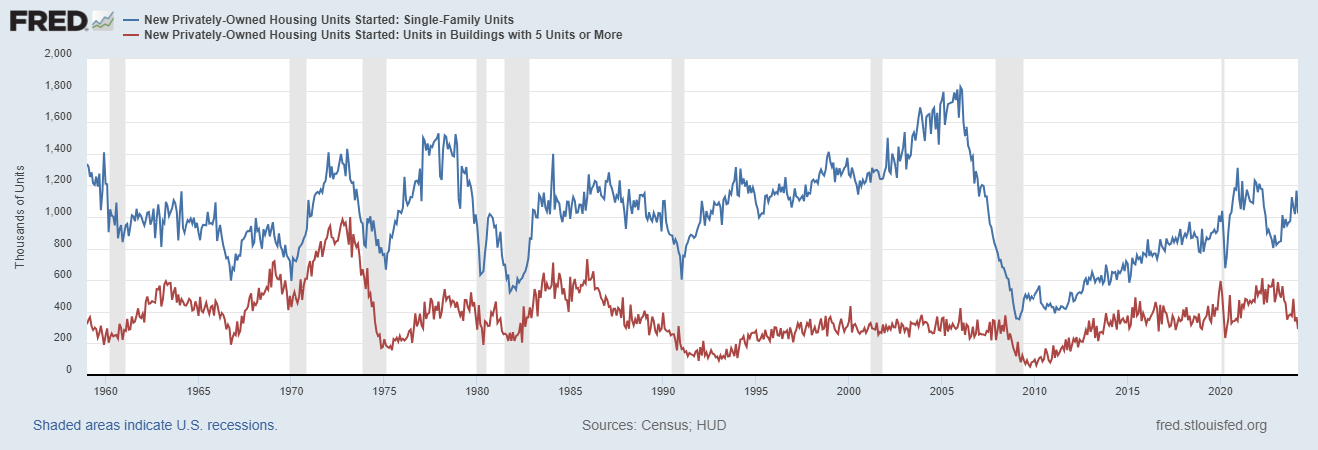

Real estate begins are expanding annual, and 5-unit begins are breaking down. In 2021, I created a critical piece mentioning that when home mortgage prices increase and building contractors begin to earn less cash structure, they will certainly fold up like they constantly do. This is a superb instance of why I state building contractors aren’t the March of Dimes.

A significant void in between real estate begins and 5-unit begins has actually been developing.

I wished to maintain this real estate begins record uncomplicated today to obtain individuals to look in advance in the future and link the dots, due to the fact that the Fed will only pivot when the labor market breaks, when they see out of work insurance claims increasing. That, consequently, will certainly bring about reduced home mortgage prices as the bond market ferrets out exact recessionary information and takes returns and home mortgage prices reduced. Up until after that, home mortgage prices and bond returns will certainly rise.

[ad_2]

Source link