[ad_1]

Marx Sterbcow, a realty legal representative and handling lawyer at Sterbcow Regulation Team, based about 40 miles north of New Orleans, insurance policy expenses have actually produced a quick run-up in his yearly costs. He paid $4,700 in 2022, $11,500 in 2023 and got a quote of $28,000 for 2024.

” I’m unsure what else can be done to decrease the expenses apart from to raise the deductibles. My residence has never ever had an insurance claim, has actually all the included bells and whistles to aid minimize versus any type of prospective insurance claim,” Sterbcow claimed.

Although Sterbcow is fairly near the coastline in the New Orleans city location, enhancing his building’s danger for storm damages, the obstacle of increasing insurance policy expenses is a statewide concern.

” There are some legal problems with insurance policy and tax obligations on insurance policy, however there is no question that we have actually had a lot more serious all-natural catastrophes,” claimed Stephen Lovecchio, the proprietor of the New Orleans branch of insurance policy company The Woodlands Financial Team “The insurer are just attempting to make a nickel on every buck, however if we need to pay for a $100 million or $200 million tornado, prices need to go up as necessary.”

Throughout the state, representatives really feel these increasing insurance policy expenses in addition to greater home mortgage prices and sale price. According to Altos Research data, 90-day typical sale price have actually increased from about $230,000 in April 2020 to $275,000 in very early April 2024, adding to the downturn in home sales.

According to data from Redfin, 2,491 homes were marketed in Louisiana in February 2024, down 6.2% year over year, and virtually the same to the 2,492 homes marketed in February 2020 before the COVID-19 pandemic.

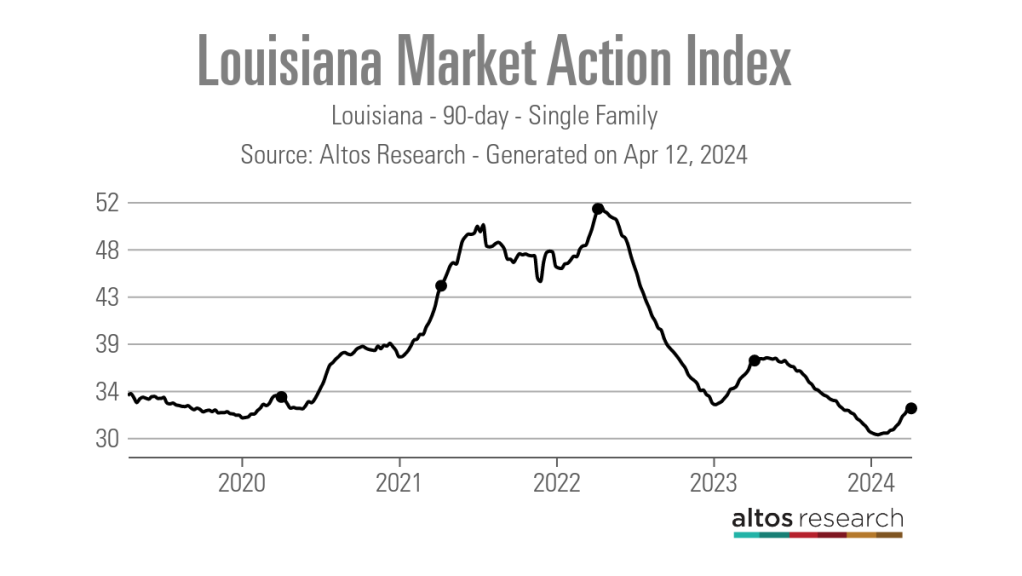

Furthermore, the state’s 90-day ordinary Altos Market Activity Index rating was 32.75 since April 5, 2024– below 37.21 one year previously, however virtually the same to ball game of 32.77 videotaped in mid-February 2020. Altos categorizes ratings over 30 to be a sign of a vendors’ market.

” Vendors will certainly desire leading buck for their building, however we are seeing purchasers beginning to check out working out points like shutting expenses or getting down their rates of interest,” claimed Jessica Huber, a Keller Williams Real Estate Front Runner representative based in Prairieville. “I have actually seen purchasers request for and obtain in between $8,000 and $10,000 in shutting expenses covered. Rates are still more than they were formerly, however at the very least in my location, vendors are dealing with purchasers.”

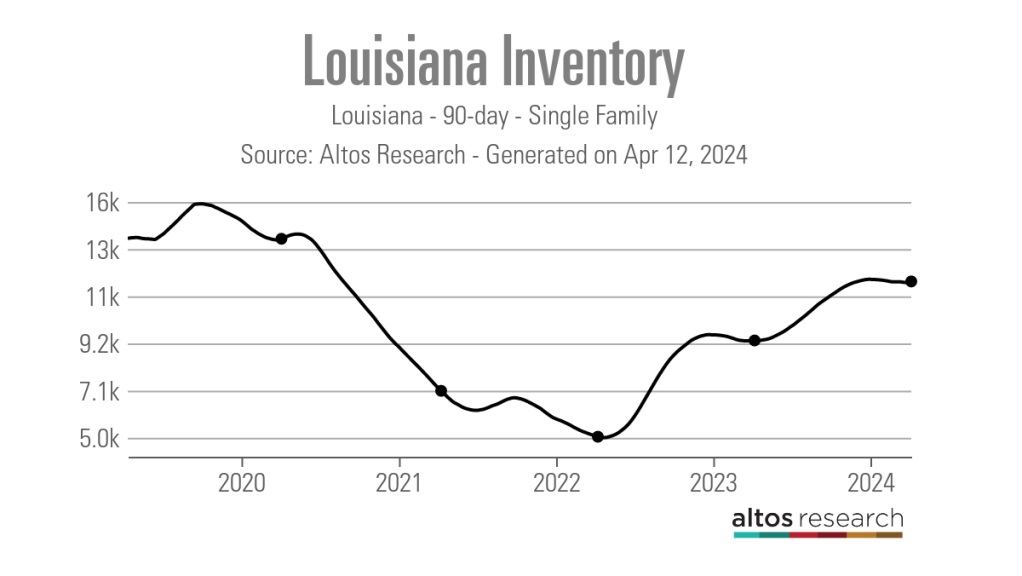

An additional indication of the slower market problems is the statewide surge in stock. After the 90-day ordinary got to a flooring of 5,010 single-family energetic listings in mid-April 2022, it has actually boosted to 12,028 since very early April 2024. In contrast, statewide stock went to 14,129 energetic listings in mid-February 2020.

While stock is plainly headed in the best instructions, neighborhood representatives state that it is still tough for purchasers at specific rate indicate locate high quality listings.

” Supply really feels rather well balanced,” claimed Josh Foster, an Departure Real Estate Southern representative based in Sulphur. “I assume we are running near regarding a six-month supply, however among things we are still encountering is that there is still not a great deal of homes in that wonderful area for the majority of purchasers– best at the $200,000 to $300,000 mark, 2 acres with 3 or 4 rooms. It’s simply not available.”

With these “wonderful area”- kind buildings, when one does begin the marketplace, Foster claimed he has actually seen some multiple-offer circumstances, however absolutely nothing like the post-pandemic rise of 2020 and 2021.

With purchase quantity slowing down, representatives are doing whatever they can to ensure the bargains they have close efficiently. For the majority of, this implies bringing a homeowners insurance agent right into the purchase rather than they made use of to.

” Currently we are obtaining the insurance policy quote prior to we also send a deal on a residence, to make sure that they understand what their complete repayment is mosting likely to be,” Johnson claimed. “It is a great deal even more research than previously, however at the very least we understand prior to we make a deal if the customer can also manage their regular monthly repayment, or perhaps if they can obtain the home mortgage due to the fact that the insurance policy costs will certainly affect their debt-to-income proportion.”

Along with assisting existing purchasers, representatives are additionally dealing with previous customers to aid them handle their home owners insurance policy expenses.

” I have actually had individuals call me to detail their residence due to the fact that they can no more manage their insurance policy. So, I have actually been educating individuals regarding the requirement to search for insurance policy,” Johnson claimed. “I have actually been lucky that I have actually had the ability to aid them locate far better prices to make sure that they can remain in their home. Your insurer does not need to be your insurer permanently.”

Although the insurance policy obstacles dealing with Louisiana’s property market will certainly not go away over night, representatives are enthusiastic for the future. Under existing state legislations, insurance policy service providers are outlawed from going down home owners that have actually been consumers for at the very least 3 years.

In late March, nonetheless, the Louisiana Legislature elected to enable insurer a lot more flexibility in going down house owner plans. The expense still requires to be gone by the state Us senate, however representatives are enthusiastic the adjustment would certainly tempt a lot more service providers to use insurance coverage in higher-risk locations, offering home owners and purchasers a lot more options.

” The reinsurers see this policy and they do not intend to become part of points in Louisiana– they do not intend to come right here,” Johnson claimed. “So, we have a scenario where we do not have competitors therefore that is increasing the rates also greater.”

Lovecchio additionally kept in mind that he anticipates insurance policy costs to decrease in the coming years.

” The brand-new insurance policy commissioner is enabling firms to elevate and reduced prices a great deal quicker, so ideally customers will certainly see much less lag time on their price adjustments,” Lovecchio claimed.

” I assume rates will certainly regulate a little bit progressing. We have actually seen them quit rising, to make sure that is great– it is the very first step. Yet we additionally wish some even more service providers will certainly enter our markets and bring them reduced due to the fact that we actually require prices to decrease.”

[ad_2]

Source link